Many business owners don’t realize that they still may need to file a tax return even if the business didn’t make any money this past year. Filing is an Extension for your business doesn’t cost anything and it’s an easy way to avoid any penalties and give you additional time to file a more accurate return.

But if you miss the deadline and don’t file an Extension, the penalties can add up quickly. Thus, business owners need to take these deadlines very seriously, pay attention to the type of business entity they have, and not trust their professional to always alert them for potential filing deadlines.

Here are the basics and I encourage you to take action and note on your calendar if necessary.

You DO NOT need to file a business tax return if you meet one of the following exceptions:

However, you DO NEED to file a business tax return if you are in one of the following situations:

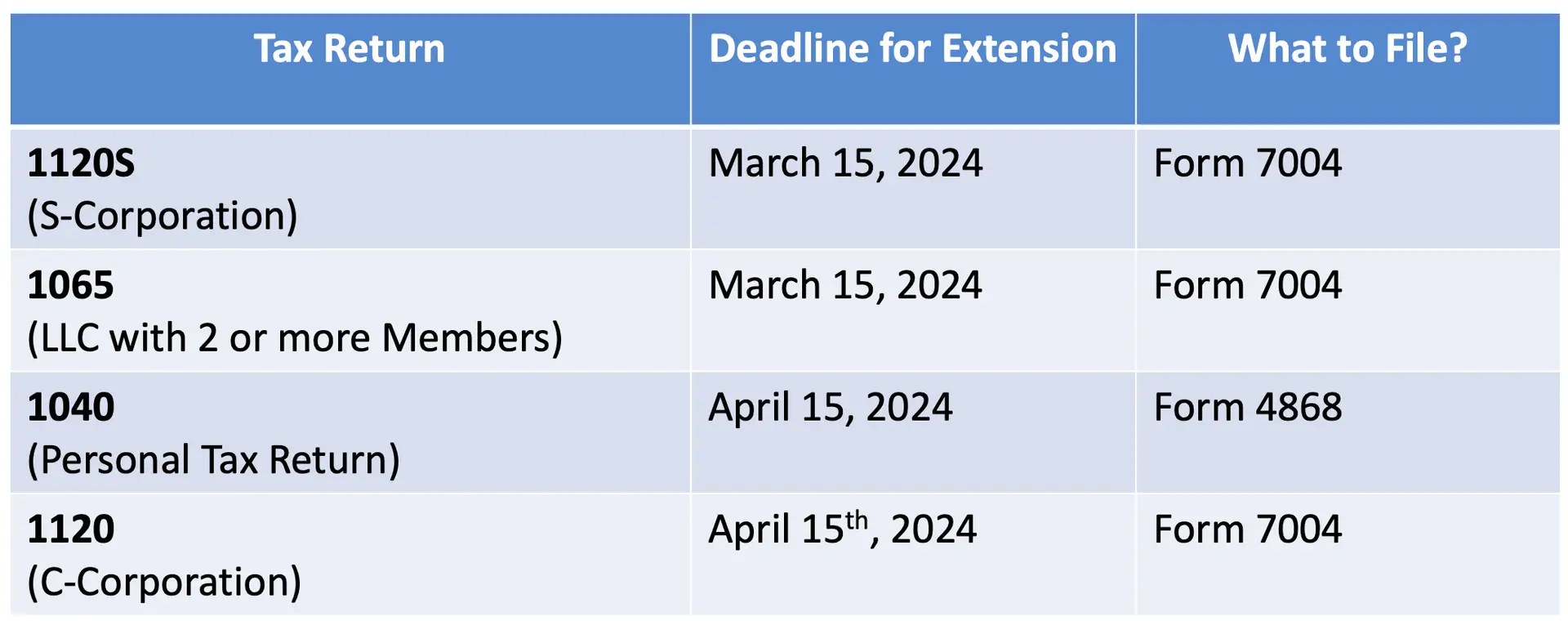

See the following table for appropriate due dates and extension deadlines:

Once you know if one or more of your businesses needs to file a separate tax return, rather than simply a schedule on your 1040, you can note your calendar and sleep calmly at night.

Please see my separate article “What to do if You Can’t Pay Your Taxes by April 15th” regarding your personal taxes and a potential extension. Needless to say, the penalties for not personal tax returns and/or extensions can add up just as quickly as a business return, if not faster.

When a Limited Liability Company (2 Members or more – MMLLC) fails to file Form 1065 by March 15th, or file an Extension – Form 7004, the IRS imposes a penalty of $220 for each month, or part thereof, up to a maximum of 12 months, multiplied by the number of Members.

For Example, if there are 2 Members and they forget to file an Extension by March 15th and file the tax return in September, the penalty would be $2,640 (6 months x $220 x 2). HOWEVER, if the LLC files an Extension (Form 7004), it gives you 6 months to file by September 15th without penalty (and there is no fee to the IRS to file an Extension).

IF the LLC files an Extension BUT doesn’t file by September 15th, the same penalty rule above starts to kick in after September 15th (not to mention the domino effect it will have on the individual Members inability to file their own personal tax return, or requirement to ‘Amend’ their tax return when they finally receive their K-1.

When an S corporation fails to file Form 1120S by March 15th, or file an Extention – Form 7004, the IRS imposes the same penalty of $220 for each month, or part thereof, multiplied by the number of Shareholders, for a maximum of 12 months.

For Example: if there are 3 shareholders and they forget to file an Extension by March 15th but file the tax return by the end of June, the penalty would be $1,890. (There’s actually could be a penalty and interest calculation on taxes that might be owed in an S-Corporation, but that is extremely rare because an S-Corporation is a pass-thru entity. However, there are some types of taxes that could be assessed, such as a built-in gains tax or something of a similar nature.)

IF the S-Corp files an Extension BUT doesn’t file by September 15th, the penalty rule above starts to kick in after September 15 (and again not to mention the domino effect it will have on the individual Shareholders and their inability to file their own personal tax return until they receive the K-1).

When a C-Corporation fails to file Form 1120 by April 15th or file an Extension – Form 7004, the penalty for late filing is a monthly penalty that’s equal to 5 percent of any income tax that remains unpaid, up to a maximum 25 percent penalty after the fifth month that the return remains unfiled. If the C-Corporation doesn’t owe any taxes (or a nominal amount), the minimum penalty for a return that is more than 60 days late is the lesser of the tax owed or $485.

If you missed filing the extension and find yourself in a predicament assessed with this Failure to File Penalty, the IRS may provide administrative relief under its “First Time Penalty Abatement Policy”.

In order to for a taxpayer to qualify, they need to be able to satisfy ALL of the following 3 tests:

As a cautionary note, keep in mind that the Failure to File Penalty continues to accrue until the tax is paid in full. It may be wise to wait until you fully pay the penalty due before requesting penalty relief under the Service’s first-time penalty abatement policy.

In summary, please make sure you act as the ‘Captain of Your Own Ship’ and be informed as to when the filing deadlines are for your business. Then note your calendar and follow up with your tax professionals with plenty of time to remedy the situation if there is something missing.

Mark J. Kohler is a CPA, Attorney, co-host of the PodCasts “The Main Street Business Podcast” and “The Directed IRA Podcast”, and the author of “The Business Owner’s Guide to Financial Freedom- What Wall Street Isn’t Telling You” and, “The Tax and Legal Playbook- Game Changing Solutions For Your Small Business Questions”, as well as several other well-known books. He is also the CFO of Directed IRA Trust Company, and a senior partner at the law firm Kyler Kohler Ostermiller & Sorensen, LLP.

{kind=link}